Quarterly Asset Remarketing Report - Q3 2020

- The Road Transport Sector continues to reduce in sales volume but shows some semblance of stabilisation after a reduction of only 13% on the same period last year.

- Delays have been extended on new stock with global production capacity reduced.

- With almost all Australian businesses now eligible for a full write-off of asset purchases manufacturers supplying business assets across road transport, automotive and machinery are seeing some rebounds in certain sectors.

- Agricultural equipment sales have continued to thrive during the third quarter, which is being driven by good seasonal weather conditions, low-interest rates, high commodity prices and tax incentives.

- The automotive sector saw year to date sales reach a total of 811,464 vehicles sold, with an overall market decline of 21.8%.

- The 2020 Nobel Prize Winner in Economic Sciences was jointly awarded to Paul Milgrom and Robert Wilson for ‘improvements to auction theory and inventions of new auction formats’.

Road Transport

Key Point Summary

- Third quarter has seen signs of stabilisation in the road transport market after a reduction of 13% on the same period last year.

- After three months of consecutive reductions in sales volumes for the heavy-duty market, September results returned to more positive territory.

- The light duty truck market outperformed both the heavy and medium duty truck market in the third quarter

New Road Transport Market

Economic conditions continue to deteriorate, with the country having been through a recession and now, according to the RBA, out of recession. The impact on the Road Transport Industry is significant, with year on year Revenue down ~$46bn and major delays occurring in the production of new stock as a result of extended delays in global manufacturing. As it currently stands, the delivery time on new trucks varies across the different brands, as highlighted in the table below.

![]()

Third quarter sales saw little change from the previous two quarters, with a total of 8,365 new trucks & vans sold. This represents some semblance of stabilisation after a reduction of 13% on the same period last year.

Heavy Duty Market

With three months of consecutive reductions in sales volume, September result returned to more positive territory, exceeding 900 registrations after ceding 821 and 782 registrations in August and July respectively

With three months of consecutive reductions in sales volume, September result returned to more positive territory, exceeding 900 registrations after ceding 821 and 782 registrations in August and July respectively

Year to date, we have continued to see Volvo be the best performer in this market with a total of 1,319 registrations, however this is a decline of 20.3% on the previous year figures. Kenworth follows at a very close second with a total of 1,316 registrations from January to September 2020, while Isuzu comes in third with only 937 registrations for this period.

Medium & Light Duty Market

The medium and light duty new truck market has continued to see declines during the third quarter, but not to the same levels that we have seen in the heavy-duty market.

The medium duty market saw 570 registrations in July, this is a 9.8% decrease on 2019 figures for the same period. This market saw a further decline in August, with a total of 484 new registrations, bringing the drop to a 24.8% over the same period in 2019. The medium duty market in September continued to record negative growth as seen throughout the rest of 2020, the overall month saw a 17.2% decrease on sales for the same period in the previous year.

Light duty trucks, whilst reporting declining sales year on year of 8% still managed to outperform both larger Road Transport markets, recording registrations of 989, 849 & 907 respectively for July, August & September.

Secondary Road Transport Market

The third quarter has seen the second hand truck market report strong results for all road transport assets, as auction clearance rates remain strong. This has been a result of the lack of stock on new and secondary road transport assets and buyer demand being driven whilst the instant tax write-off is still available to them.

Queensland has seen a drop in the number of trucks on offer at auctions house since the onset of COVID-19. This is helping to drive the strong prices and clearance rates at auction as highlighted in the sale of a 2016 Hino 700 Series Prime Mover with 264,386kms for $85,000, achieving 100% of retail value and a 2016 Volvo FM Prime Mover with 398,404kms for $106,000, achieving 95% of retail value.

European trucks in the Victorian market have continued to be a popular purchase amongst buyers during the third quarter and we have seen an increase in competitive metro contracts that has increased freight movements within the state.  As a result of this, we have seen a marginal improvement in the Prime Mover market late in the third quarter within Victoria, as shown with the August sale of a 2018 Volvo FH16 600HP 6×4 Prime Mover with 374,255kms selling for $185,000 and achieving 90% of retail value, the July sale of a 2002 Kenworth T404 Prime Mover with 853,825kms selling for $27,700 and achieving value and a 2012 Mercedes Actros 1841 6×4 Prime Mover with 343,609 kms selling for $34,000 and achieving 80% of retail value. The third quarter has seen a shortage of heavy haulage trucks and side tippers in the Western Australian market due to the numerous mining and civil contracts that are underway nationally. Light and medium duty trucks in this market have continued to perform well, as evidenced by the following results of a 2010 Isuzu NLR200 with 183,020 kms selling for $17,050 and a 2010 Hino Fridge Truck with 217,418 kms selling for $13,000, both of these trucks achieved 80% of retail value.

As a result of this, we have seen a marginal improvement in the Prime Mover market late in the third quarter within Victoria, as shown with the August sale of a 2018 Volvo FH16 600HP 6×4 Prime Mover with 374,255kms selling for $185,000 and achieving 90% of retail value, the July sale of a 2002 Kenworth T404 Prime Mover with 853,825kms selling for $27,700 and achieving value and a 2012 Mercedes Actros 1841 6×4 Prime Mover with 343,609 kms selling for $34,000 and achieving 80% of retail value. The third quarter has seen a shortage of heavy haulage trucks and side tippers in the Western Australian market due to the numerous mining and civil contracts that are underway nationally. Light and medium duty trucks in this market have continued to perform well, as evidenced by the following results of a 2010 Isuzu NLR200 with 183,020 kms selling for $17,050 and a 2010 Hino Fridge Truck with 217,418 kms selling for $13,000, both of these trucks achieved 80% of retail value.

The lack of stock available in the secondary market has driven up prices achieved at auction throughout the New South Wales market in the third quarter as shown in the sale of a 2010 Hino FY 700 8×4 Tipper with 458,876kms selling for $97,500, achieving 93% of retail and a 2007 Isuzu FVZ 1400 6×4 Tabletop with Hiab 200C-4 Crane with 275,177kms selling for $65,000, achieving 90% of retail value, both of these assets would have sold for substantially less 6 months ago. This is correlated to the 3 to 6-month delay for new road transport stock, as it has impacted on dealer’s ability to complete trades and fill their yards with secondary assets. With this in mind, we are seeing both end users and dealers battling it out at auctions to fulfil their requirements in this market and driving the upward pressure on prices.

The lack of stock available in the secondary market has driven up prices achieved at auction throughout the New South Wales market in the third quarter as shown in the sale of a 2010 Hino FY 700 8×4 Tipper with 458,876kms selling for $97,500, achieving 93% of retail and a 2007 Isuzu FVZ 1400 6×4 Tabletop with Hiab 200C-4 Crane with 275,177kms selling for $65,000, achieving 90% of retail value, both of these assets would have sold for substantially less 6 months ago. This is correlated to the 3 to 6-month delay for new road transport stock, as it has impacted on dealer’s ability to complete trades and fill their yards with secondary assets. With this in mind, we are seeing both end users and dealers battling it out at auctions to fulfil their requirements in this market and driving the upward pressure on prices.

Secondary Trailer Market

We have seen the same trends in the secondary trailer market across the country as we have in the secondary truck market, with assets performing well due to the lack of stock available across the country, with lead times for new trailers extending out to 3 months and a country-wide increase in metro contracts for delivery of freight and parcels.  Examples of the strength in the secondary market can be seen from the sale of a 2015 Krueger High Cube Curtainsider Trailer and 2014 Vawdrey Drop deck trailers selling for $55,600 and $59,9000 respectively and achieving 100% of retail value in our August truck and machinery auction in Melbourne. Further examples of the strength in the secondary trailer market can be seen in the sale of a 2011 Vawdrey VB S3 Drop Deck Curtainsider Trailer that sold for $28,000 in our Queensland truck and machinery, this achieved 100% of retail value. In Western Australia we saw similar results with the sale of a 2016 Vawdrey VBS3 Curtainsider selling for $60,000 and a 2018 AAA Drop Deck extendable Trailer telling for $60,000, these have achieved 100% of retail value.

Examples of the strength in the secondary market can be seen from the sale of a 2015 Krueger High Cube Curtainsider Trailer and 2014 Vawdrey Drop deck trailers selling for $55,600 and $59,9000 respectively and achieving 100% of retail value in our August truck and machinery auction in Melbourne. Further examples of the strength in the secondary trailer market can be seen in the sale of a 2011 Vawdrey VB S3 Drop Deck Curtainsider Trailer that sold for $28,000 in our Queensland truck and machinery, this achieved 100% of retail value. In Western Australia we saw similar results with the sale of a 2016 Vawdrey VBS3 Curtainsider selling for $60,000 and a 2018 AAA Drop Deck extendable Trailer telling for $60,000, these have achieved 100% of retail value.

| Assets | Kms/Hours | Price Achieved | % of retail | State |

|---|---|---|---|---|

| 2015 Krueger High Cube Curtainsider B Trailer | 333,649 | $55,600 | 100% | VIC |

| 2014 Vawdrey 45FT Drop Deck Curtainsider | $59,900 | 100% | VIC | |

| 2012 TCA 45FT Tri Axle Refrigerated Trailer | $47,700 | 100% | VIC | |

| 2016 Hino 700 Series Prime Mover | 264,386 | $85,000 | 100% | QLD |

| 2011 Vawdrey VB S3 Drop Dreck Curtainsider Trailer | $28,000 | 100% | QLD | |

| 2014 Gippsland Body Builders A&B Tipper Set | $88,000 | 100% | QLD | |

| 2016 Vawdrey VBS3 Curtainsider | $60,000 | 100% | WA | |

| 2018 AAA Drop Deck Extendable Trailer | $60,000 | 100% | WA | |

| 2016 Volvo FM Prime Mover | 398,404 | $106,000 | 95% | QLD |

| 2009 Kenworth T658 Prime Mover | 1,006,328 | $66,200 | 95% | QLD |

| 2018 Krueger ST-3-38 Curtainsider Trailer | $52,000 | 95% | QLD | |

| 2015 MAN TGX26.540 6x4 | 501,207 | $65,100 | 95% | WA |

| 2010 Hino FY 700 8x4 Tipper | 458,876 | $97,500 | 93% | NSW |

| 2018 Volvo FH16 600HP 6x4 Prime MOver374,255 | 374,255 | $185,000 | 90% | VIC |

| 2012 Western Star 4964 FX Prime Mover | 754,084 | $50,000 | 90% | QLD |

| 2011 Mack CSMR 8x4 Watercart | 145,692 | $82,400 | 90% | WA |

| 2007 Isuzu FVZ 1400 6x4 Tabletop with Hiab 200C-4 Crane | 275,177 | $65,000 | 90% | NSW |

| 2013 Fino FD 500 Tilt Tray | 293,292 | $82,400 | 89% | VIC |

| 2016 Hino 300 716 Tabletop | $30,050 | 86% | NSW | |

| 2013 Maxitrans ST3 Tri-Axle 30FT Tipper Trailer | $64,300 | 86% | VIC | |

| 2010 Volvo FM13 6x4 Euro | 653,826 | $47,900 | 85% | NSW |

| 2018 Isuzu NLR 45-150 | 22,032 | $30,200 | 85% | NSW |

Mining & Earthmoving

Key Point Summary

- Caterpillar Inc. saw profits in the third quarter decline by 63% in comparison to the same period in 2019.

- Results for equipment sales have been a mixed bag, with Victoria being the worst performer.

- Auction results have remained strong for equipment sales in the secondary market.

New Earthmoving & Mining Market

Caterpillar Inc. saw profits decrease by 63% in comparison to the same period in 2019, this has been driven by lower end-user demand for equipment and service. Revenue increased 14% in the Asia/Pacific region for the construction industries as a result of the changes in dealer inventories and increased sales within China. Caterpillar Inc. resources industries saw revenue decrease by 13% and the energy and transportation’s revenue decrease by 33%.

With almost all Australian businesses now eligible for a full write-off of asset purchases, up to any value, the construction industry is reporting that activity is picking up in ‘virus-free’ states, while conditions in Victoria sink to record lows.

The monthly Australian Performance of Construction Index (Australian PCI), adjusted by the Australian Industry Group and Housing Industry Association,

increased by 7.3 points to 45.2 in September, indicating improving conditions in the sector albeit still in contraction.

Readings below 50 points indicate contraction in activity, with lower results indicating a faster rate of contraction. On the other hand, readings above 50 indicate growth.

Secondary Earthmoving & Mining Market

During the third quarter, we have seen strong auction results for secondary earthmoving and mining equipment that has been presented for sale. The driving factors behind these results is the Government stimulus program, made up from the $150,000 instant asset write off program, new infrastructure projects and continuation of existing projects. We have also seen a drop in the Australian Dollar in comparison to the US Dollar, this pushes up the price for new imported equipment and drives consumers to purchase good quality machines that are available on the secondary market instead.

In Victoria, there has been a flow of enquiries coming in for various sized earthmoving equipment during the quarter, particularly an increase in enquiries from sole traders who are chasing smaller machines. This has been reflected in the auction results, where we saw a 2018 Case CX130C with 2,424 hours showing, selling for $115,600 (100% of retail value). In addition to this, we saw a 2004 CAT 12H Grader with 18,520 hours presented for sale throughout the quarter, which was purchased for $76,200 (80% of retail value), this machine was bought by a dealer who was looking to export it to Asia.

In Victoria, there has been a flow of enquiries coming in for various sized earthmoving equipment during the quarter, particularly an increase in enquiries from sole traders who are chasing smaller machines. This has been reflected in the auction results, where we saw a 2018 Case CX130C with 2,424 hours showing, selling for $115,600 (100% of retail value). In addition to this, we saw a 2004 CAT 12H Grader with 18,520 hours presented for sale throughout the quarter, which was purchased for $76,200 (80% of retail value), this machine was bought by a dealer who was looking to export it to Asia.

Mining equipment in the secondary market across New South Wales has remained stable throughout the third quarter with many owners continuing work as normal or reducing/increasing utilization as required for their units, this was highlighted through the sale of a Caterpillar D11T Dozer that achieved 90% of retail value at auction. Earthmoving equipment in the New South Wales market has continued to obtain strong prices for all equipment offered for sale, this can be seen in the sale of a 2013 Case CX210B Excavator that for 90% of retail value at auction. Just prior to the COVID-19 pandemic, we would have seen this asset sell for 15% less.

Another example of the strong results on this market is the sale of a circa 2003 Caterpillar D5G Dozer, that sold for a 100% of retail value at auction, despite this machine needing a bit of attention and servicing.

Western Australia has also continued to see the good results in the secondary earthmoving and mining equipment sector in the third quarter of 2020. This has been highlighted in the results of a 2017 Caterpillar 320FL Excavator with 4,859 hours showing selling for $215,000 and achieving 100% of retail value. Queensland has also seen these strong results throughout the quarter, this has been highlighted in the sale of a 2018 Hitachi ZX225US LC-5B Hydraulic Excavator with 2,278 hours showing, selling for $191,200 and achieving 120% of retail value.

| Assets | Kms/Hours | Price Achieved | % of retail | State |

|---|---|---|---|---|

| 2018 Hitachi ZX225US LC-5B Hydraulic Excavator | 2,278 | $191,200 | 120% | QLD |

| 2001 Caterpillar 627G Motor Scraper | 20,087 | $225,000 | 110% | QLD |

| 2011 Caterpillar 12M Motor Grader | 7,954 | $178,000 | 105% | QLD |

| 2018 CASE CX130C 13T Tracked Excavator | 2,424 | $115,600 | 100% | VIC |

| 2012 Caterpillar D6T XL Crawler Tractor | 8,225 | $259,200 | 100% | QLD |

| Circa. 2003 Caterpillar D5G LGP Dozer | 26,753 | $72,000 | 100% | NSW |

| 2017 Caterpillar 320FL Excavator | 4,859 | $215,000 | 98% | WA |

| 2008 Caterpillar 980H Wheel Loader | 13,899 | $125,000 | 95% | QLD |

| 2016 Komatsu PC-138US-8 Crawler | 2,922 | $110,100 | 92% | NSW |

| 2012 McCloskey International S190 Screener | 5,732 | $175,400 | 90% | QLD |

| 2013 CASE CX210B Tracked Excavator | 6,218 | $45,100 | 90% | NSW |

| 2014 Takeuchi TB216 Mini Excavator | 900 | $17,600 | 90% | NSW |

| Bobcat T770 | 155 | $90,000 | 90% | NSW |

| 2017 CAT 259D Skid Steer Loader | 1,500 | $70,200 | 89% | VIC |

Agriculture

Key Point Summary

- The agriculture equipment sales sector has been driven by good seasonal weather conditions, low interest rates, high commodity prices and government tax incentives.

- New South Wales saw the largest increase in new tractor sales throughout the quarter.

- Secondary agriculture equipment sales continue to remain strong due to strong environmental conditions.

New Agriculture Market

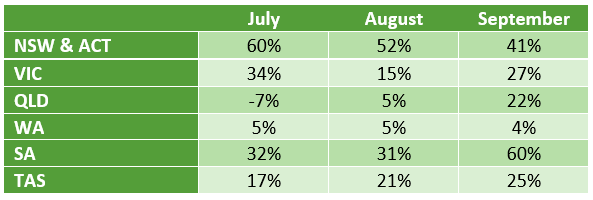

Agricultural equipment sales have continued to thrive during the third quarter, with this industry being driven by good seasonal weather conditions, low interest rates, high commodity prices and the government tax incentives previously mentioned. There have been strong results for new tractor sales across the country, with overall sales increasing by 24% in July, on the same period 2019. Highlighted in the table below we can see that New South Wales had the largest increase in new tractor sales in July with a 60% increase on the same period of 2019, followed closely by Victoria and South Australia. In August these trends continued with the over all market up 19% on the same period of 2019 and September was no different with another rock solid month and tractor sales increasing 29% on the same period in 2019.

Agricultural equipment sales have continued to thrive during the third quarter, with this industry being driven by good seasonal weather conditions, low interest rates, high commodity prices and the government tax incentives previously mentioned. There have been strong results for new tractor sales across the country, with overall sales increasing by 24% in July, on the same period 2019. Highlighted in the table below we can see that New South Wales had the largest increase in new tractor sales in July with a 60% increase on the same period of 2019, followed closely by Victoria and South Australia. In August these trends continued with the over all market up 19% on the same period of 2019 and September was no different with another rock solid month and tractor sales increasing 29% on the same period in 2019.

Most of the strength in the new tractor market has been for small machines in the 40hp range, this sector saw sales increase by 71%. Demand for new larger tractors have been impacted by the drought, with recent price increases for to purchase machinery and supply chain issues. Combine Harvesters have been purchased and placed for the upcoming harvest season; this saw sales remaining steady for the quarter. It is forecasted that the likely outcome for the overall combine harvester sales for 2020 will see a total increase of 15-20% on 2019 results. Baler sales have continued to remain strong throughout the quarter, with overall sales up 33% year to date.

Secondary Agriculture Market

The secondary agricultural market has seen limited assets come to hand across the country during the third quarter as stock has been hard to come by. Prices for these assets have remained strong across the country as strong environmental conditions for farmers have remained positive. Examples of the strength of the market across the country can be seen in the sales of recent machines at our auctions.

The secondary agricultural market has seen limited assets come to hand across the country during the third quarter as stock has been hard to come by. Prices for these assets have remained strong across the country as strong environmental conditions for farmers have remained positive. Examples of the strength of the market across the country can be seen in the sales of recent machines at our auctions.

In New South Wales, we sold a 2017 Landini REX 90F Front Wheel Assist Tractor, this machine sold for 90% of retail value and fetched $38,750. In Victoria we sold a 2011 John Deere 6230E Tractor with 5,779 kms showing for $39,400 and a 2013 Massey Ferguson 5450 Tractor with 6,449 hours for $42,000 in Queensland, both units achieved 90% of retail value.

In Western Australia, we are seeing Sheep continued to be trucked to the Eastern states, with 41,000 sheep and lambs crossing the border in August alone. Due to this we are seeing higher demand for agricultural stock trailers across the country, and this was highlighted in a Queensland auction, where we sold a 2010 Hino F700 Cattle Truck with 980,431 kms for $73,200 and achieved 105% of retail value.

In Western Australia, we are seeing Sheep continued to be trucked to the Eastern states, with 41,000 sheep and lambs crossing the border in August alone. Due to this we are seeing higher demand for agricultural stock trailers across the country, and this was highlighted in a Queensland auction, where we sold a 2010 Hino F700 Cattle Truck with 980,431 kms for $73,200 and achieved 105% of retail value.

| Assets | Kms/Hours | Price Achieved | % of retail | State |

|---|---|---|---|---|

| 2010 Hino F700 Cattle Truck | 980,431 | $73,200 | 105% | QLD |

| 2014 Goldacres G4 4036 Self Propelled Sprayer | 5,083 | $115,500 | 95% | QLD |

| 2011 Claas Lexion 740 Header & Macdon D-65 40 Foot Front | 2,514 | $141,250 | 95% | QLD |

| 1998 Caterpillar Challenger 95E Tractor | 6,473 | $50,000 | 95% | QLD |

| 2011 Case Magnum 315 FWA Tracto | 5,505 | $97,500 | 95% | QLD |

| 2011 John Deere 6230E Tractor | 5,779 | $39,400 | 90% | VIC |

| 2013 Massey Ferguson 5450 Tractor | 6,449 | $42,000 | 90% | QLD |

| 2017 Landini Rex FWA 90G Tractor | 326 | $38,750 | 90% | NSW |

Aviation

Aviation data continues to show a significant contraction in global demand. The International Air Transport Association (IATA) has reported that the calendar year fall is expected to be 66 per cent, which is higher than

the forecast 63 percent. IATA reported that global domestic traffic (measured in revenue passenger kilometres) fell 50.9 percent in August.

The federal government has extended budget support for two aviation programs which support major domestic routes and to regional and remote communities. The Domestic Aviation Network Support (DANS) has been extended until 31 January, and the Regional Airline Network Support (RANS) program has been extended until 28 March. The government has also announced a commitment to injecting a further $250 million into boosting regional tourism.

The certainty of flights to regional areas of aircraft operators with a tourism focus is expected to assist with passenger number for a greater number of tourist flights. Whilst we have been advised that operators along the east coast have reduced in capacity of tourist flights, some operators in Western Queensland are having one of their best years in a long time.

Automotive

Key Point Summary

- New vehicle sales continued to struggle across the country in the third quarter, with Victoria being the worst performing state.

- States that have virtually eradicated COVID-19, saw vehicle sales increase during September.

- Secondary car market sales remained strong, however have been impacted by the lack of stock available on the market.

New Automotive Market

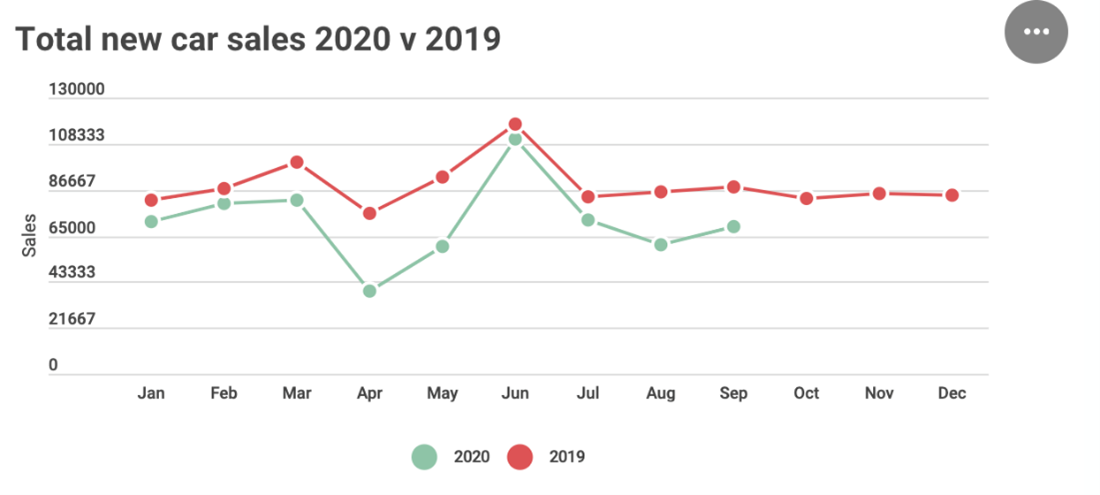

Tighter lending restrictions, bushfires and COVID-19 are some of the challenges the new automotive market has faced over the last couple of years. The third quarter of 2020 is no different, as we continue to see sales for new vehicles continuing to struggle across the country as the light at the end of the tunnel begins to come through.

Victoria was the hardest hit state for the quarter with the market down 27.8% in July, 65.9% in August and 58% in September for new car sales for the same periods in 2019. This correlates to the stage four lockdowns which saw many car dealerships across the state left empty and closed. On the other hand, we have seen states or territories that have virtually eradicated COVID-19 increase their sales for September 2020, with Australian Capital Territory up 3.4%, Northern Territory sales increased by 10.6% and Western Australia saw an increase of 1.5% on the same period in 2019.

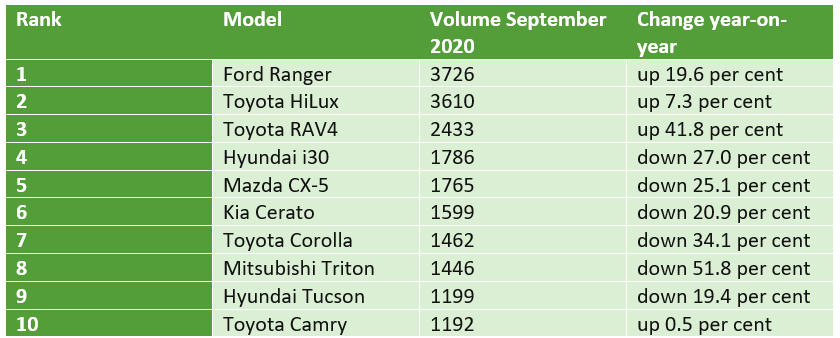

Drilling down to the bestselling models. Top 10 selling cars in September 2020.

SUV’s continue to dominate the market with passenger cars and then light commercial following.

Overall, there has been a decline in sales nationally on the same periods in 2019 with July reporting a decline of 12.8%, August dropped 28.8% and September sales decreased by 20.5%. Year to date there has been a total of 811,464 vehicles sold, with an overall market decline of 21.8%.

Secondary Automotive Market

Vehicles that are being sold on the secondary automotive market have continued to attract strong results throughout the quarter, largely due to the lack of stock that is available to buyers. Vehicles that are selling between $5,000 and $9,000 price bracket continue to perform well, this has been attributed to the early release of $10,000 from superannuation funds.

Vehicles that are being sold on the secondary automotive market have continued to attract strong results throughout the quarter, largely due to the lack of stock that is available to buyers. Vehicles that are selling between $5,000 and $9,000 price bracket continue to perform well, this has been attributed to the early release of $10,000 from superannuation funds.

While Victoria was struggling through stage four lockdown throughout the third quarter, auction results within the state remained strong as they achieved a 97% clearance rate for the quarter. Results that highlight this is the sale of a 2018 Volvo XC90 with 41,511 kms selling for $68,100, 2017 Toyota Landcruiser GXL with 82,506 selling for $70,300 and a 2017 Holden Colorado LS Dual Cab Ute with 47,206 kms selling for $34,100. Each of these vehicles achieved 100% of retail value.

Within New South Wales, we have seen rental car companies that were looking to offload their stock at the beginning of the COVID pandemic reach out in an attempt to re-purchase large stocks of second hand cars in preparation for the Christmas holiday season, as they are unable to fill these numbers with new vehicles due to the lack of stock available in this market. There has been an increase with small car dealers purchasing damaged cars for more than they are worth, if they have not been listed as a repairable write off – an example of this was 2019 Hyundai i30 that was valued at $6,000 and sold at auction for $9,000.

Within New South Wales, we have seen rental car companies that were looking to offload their stock at the beginning of the COVID pandemic reach out in an attempt to re-purchase large stocks of second hand cars in preparation for the Christmas holiday season, as they are unable to fill these numbers with new vehicles due to the lack of stock available in this market. There has been an increase with small car dealers purchasing damaged cars for more than they are worth, if they have not been listed as a repairable write off – an example of this was 2019 Hyundai i30 that was valued at $6,000 and sold at auction for $9,000.

Western Australia have reported an increase in the number of private consumers, looking to sell their cars at auction during the third quarter as they continue to see prices achieved at auction for secondhand cars remaining strong. This has been highlighted in the sale of a 2018 Toyota Hilux SR (4×4) with 99,336 kms selling for $41,400 and a 2013 Jeep Grand Cherokee SRT with 102,837 kms selling for $43,600 – both vehicles achieved a 100% of retail value.

| Assets | Kms/Hours | Price Achieved | % of retail | State |

|---|---|---|---|---|

| 2008 Holden SS Ute | 36,386 | $22,700 | 120% | NSW |

| 2019 Toyota Landcruiser VX Dual Cab | 46,298 | $71,500 | 110% | QLD |

| 2018 Jeep Grand Cherokee SRT | 33,599 | $74,100 | 105% | VIC |

| 2018 Toyota Landcruiser PRado VX | 39,183 | $60,600 | 105% | QLD |

| 2019 Toyota Landcruiser Sahara | 34,444 | $106,200 | 105% | QLD |

| 2018 Volvo XC90 D5 Inscription (AWD) | 41,511 | $68,100 | 100% | VIC |

| 2017 Toyota Landcruiser GXL (4X4) | 82,506 | $70,300 | 100% | VIC |

| 2017 Holden Colorado LS (4x4) Dual Cab | 47,206 | $34,100 | 100% | VIC |

| 2017 Isuzu D-Max SX (4x4) | 26,643 | $35,600 | 100% | VIC |

| 2018 Holden Colorado LS-X Dual Cab | 21,937 | $38,009 | 100% | QLD |

| 2017 Holden Colorado LTZ | 60,107 | $34,500 | 100% | QLD |

| 2018 Toyota Hilux SR Dual Cab | 49,473 | $38,500 | 100% | QLD |

| 2016 Mitsubishi Triton GLX (4x4) | 54,378 | $25,602 | 100% | NSW |

| 2013 Toyota Hilux SR (4x4) Dual Cab | 214,558 | $26,100 | 100% | NSW |

| 2016 Toyota Hilux Work Mate | 77,920 | $17,700 | 100% | NSW |

| 2015 HSV Gen F GTS | 47,7333 | $84,400 | 100% | WA |

| 2018 Toyota Hilux SR (4x4) | 99,336 | $41,400 | 100% | WA |

| 2017 BMW X5 30d X-Drive | 48,795 | $69,600 | 100% | WA |

| 2013 Jeep Grand Cherokee SRT | 102,837 | $43,600 | 100% | WA |

The quest for the perfect auction

The winner of the 2020 Nobel Prize in Economic Sciences in Memory of Alfred Nobel was awarded for improvements to auction theory and inventions of new auction formats

Every day, auctions distribute astronomical values between buyers and sellers. This year’s Laureates, Paul Milgrom and Robert Wilson, have improved auction theory and invented new auction formats, benefitting sellers, buyers and taxpayers around the world.

Every day, auctions distribute astronomical values between buyers and sellers. This year’s Laureates, Paul Milgrom and Robert Wilson, have improved auction theory and invented new auction formats, benefitting sellers, buyers and taxpayers around the world.

Using auction theory, it is possible to explain how these three factors govern the bidders’ strategic behaviour and thus the auction’s outcome. The theory can also show how to design an auction to create as much value as possible. Both tasks are particularly difficult when multiple related objects are auctioned off at the same time. This year’s Laureates in Economic Sciences have made auction theory more applicable in practice through the creation of new, bespoke auction formats.